Self-Employed & Buying Property? Why Your Tax Strategy Could Cost You a Mortgage

For many self-employed people in Canada, the goal is simple: minimize taxable income to keep more cash within the corporation or to reinvest in the next project. While this is a brilliant tax strategy, it creates a massive issue when it's time to close on a pre-construction unit, refinance an existing property, or even renew a mortgage.

If your tax returns show you only made $30,000 last year because you "wrote everything off," a bank will look at that $30,000 and conclude you cannot afford a million-dollar mortgage – regardless of how much cash is sitting in your business account.

The Two-Year Rule: Why You Need to Plan Ahead

Mortgage lenders (specifically "A" lenders like the Big Five banks) typically require two years of consistent, reported personal income to qualify a self-employed borrower. They don't just look at your most recent year; they take a two-year average of your reported earnings to ensure your income is stable.

So if you have a pre-construction closing coming up in 2027, you need to start paying yourself a "decent wage" now. Waiting until right before your closing is a common mistake that leads to declined applications, being forced into high-interest private lending, and a lot of unnecessary stress!

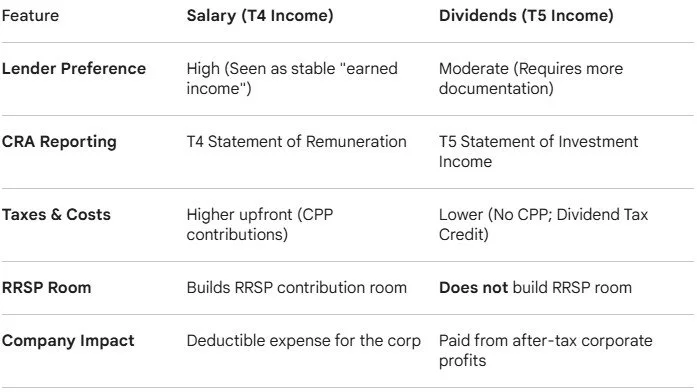

Salary vs. Dividends: Choosing Your Pay Structure

As an incorporated investor, you have two primary ways to move money from your corporation to your personal pocket. Both have pros and cons regarding mortgage qualification and tax efficiency but both will be taken into consideration for mortgage qualification.

1. Salary

Paying yourself a salary is the "cleanest" way to qualify for a mortgage. Lenders love T4 income because it is predictable and includes Canada Pension Plan (CPP) contributions. However, you (as the employer) and you (as the employee) must both pay into CPP, which can feel like an extra tax burden.

2. Dividends

Dividends are often more tax-efficient because they aren't subject to CPP and benefit from the Dividend Tax Credit. While most lenders will accept dividend income, they often want to see a longer history of consistency and may require your full corporate financial statements to ensure the business can afford to keep paying those dividends.

NOTE: Consult with an accountant for professional accounting advice on the best way to pay yourself given your situation.

Summary Checklist for Investors

If you own real estate or purchased a pre-construction unit, follow these steps to stay "mortgage ready":

Project Your Target Mortgage: Work with a broker to find out exactly how much personal income ($100k? $150k?) you need to report to qualify for the loan amount you need.

Start the Clock: Ensure you have at least two full years of that income on your Notices of Assessment (NOAs) from the CRA.

Mind the Average: If your income fluctuates, remember that lenders will average the last two years. A $0 year and a $200k year might only count as $100k in the eyes of a bank (or less).

Pay Your Taxes: Lenders will not approve a mortgage if you have outstanding personal, or corporate tax debt so keep your HST and Income Tax filings current. You will likely be required to pay off any outstanding debts like this before qualifying for a mortgage.

How Much Income Do You Need to Report?

The best way to understand how much you need to pay yourself is to work with a mortgage broker to run the numbers for you. Generally, to qualify, your total housing costs shouldn't exceed 39% of your gross income (Gross Debt Service Ratio), and your total debt (including cars/credit cards) shouldn't exceed 44% (Total Debt Service Ratio).

1) If you have NO other personal debt:

To cover that $3,125 monthly housing cost, you need a gross personal income of approximately $96,200 per year.

If you only report $40,000 to "save on taxes," you are roughly $56,000 short of qualifying for this mortgage.

2) If you have personal debt (e.g., $500/mo car payment):

Your required income jumps to approximately $100,000 per year to stay within the 44% TDS limit.

The 2-Year Strategy

Because lenders average your last two years of Notice of Assessments (NOAs), you cannot simply pay yourself $100,000 the month before you buy. Banks love to see consistency so pay yourself a consistent amount each year:

Year 1: Pay yourself $100,000.

Year 2: Pay yourself $100,000.

Result: A clean 2-year average of $100k that an "A" lender will accept.

If you paid yourself $30,000 in Year 1 and $100,000 in Year 2, the lender sees an average of $65,000—which would likely result in a declined application for a $500,000 home.

Summary

The "lean" lifestyle that serves you so well during tax season is the same thing that prevent you from qualifying for a mortgage. In the world of Canadian mortgage lending, reported income is king. If you want to scale your portfolio, close on that pre-construction unit, or unlock equity from your existing properties, you have to play the long game.

The clock is ticking on your next closing. Don't wait until the appraisal is ordered to realize your income doesn't match your ambitions.

_____

Kyle Dovigi

Real Estate Broker | CondoMillionaire.com

Anyone can become a Condo Millionaire - it all starts with one.

Real Talk. Honest Advice.

Want to work with a professional who will give you honest advice?